Welcome to this week's edition of The Finance Gem 💎 where I bring you my unabbreviated Linkedin posts you loved - so you can save them, and those posts you missed - so you can enjoy them.

This newsletter edition is brought to you by FlowCog, an incredible financial modeling tool just for SaaS companies. FlowCog will help you produce credible projections without the hassle of a spreadsheet, and get real insight into your growth trajectory for more informed decisions. FlowCog will make those board and investor calls a lot less painful, with SaaS benchmarking and what-if analysis. Try it free for 14 days, and onboard quickly with the help of a CPA and SaaS finance expert. And check out their blog for SaaS financial modelling and planning insights.

This week's highlights at a glance:

Without further ado, let's begin:

Do you know your break-even point?

Here are 10 things you need to know about breaking even:

1️⃣ When your company's revenues equal its expenses, it's neither making nor losing money, so it's said to be breaking even.

2️⃣ The break-even point occurs when revenues equal costs.

Calculating the break-even point allows you to determine the level of sales needed to cover all costs (fixed and variable) and start earning a profit.

3️⃣ The Break-Even Point can be specifically calculated in terms of both revenue dollars and/or unit numbers.

4️⃣ The Break-Even Point Formulas are:

✅Break-even (units) = Fixed cost / CM per unit

✅Break-even (dollars) = Fixed cost / CM ratio

5️⃣ Contribution Margin (CM) calculates the incremental profit in dollars earned on each sale.

The Contribution Margin formulas are:

✅Contribution margin per unit CM = Selling price per item – Variable costs per item

✅Contribution margin ratio (CM ratio) = CM/Sales Price

6️⃣ When calculating the break-even point, you need to round up to the next full unit of product or selling price, because you can't sell part of a unit, and until you sell that full unit you will not have broken even.

7️⃣ There are two main types of expenses/costs: fixed and variable.

A fixed cost doesn't change with revenues.

A variable cost, on the other hand, will change as your business sells more or fewer items.

There are also step costs, which are fixed up to a certain activity threshold, after which they change.

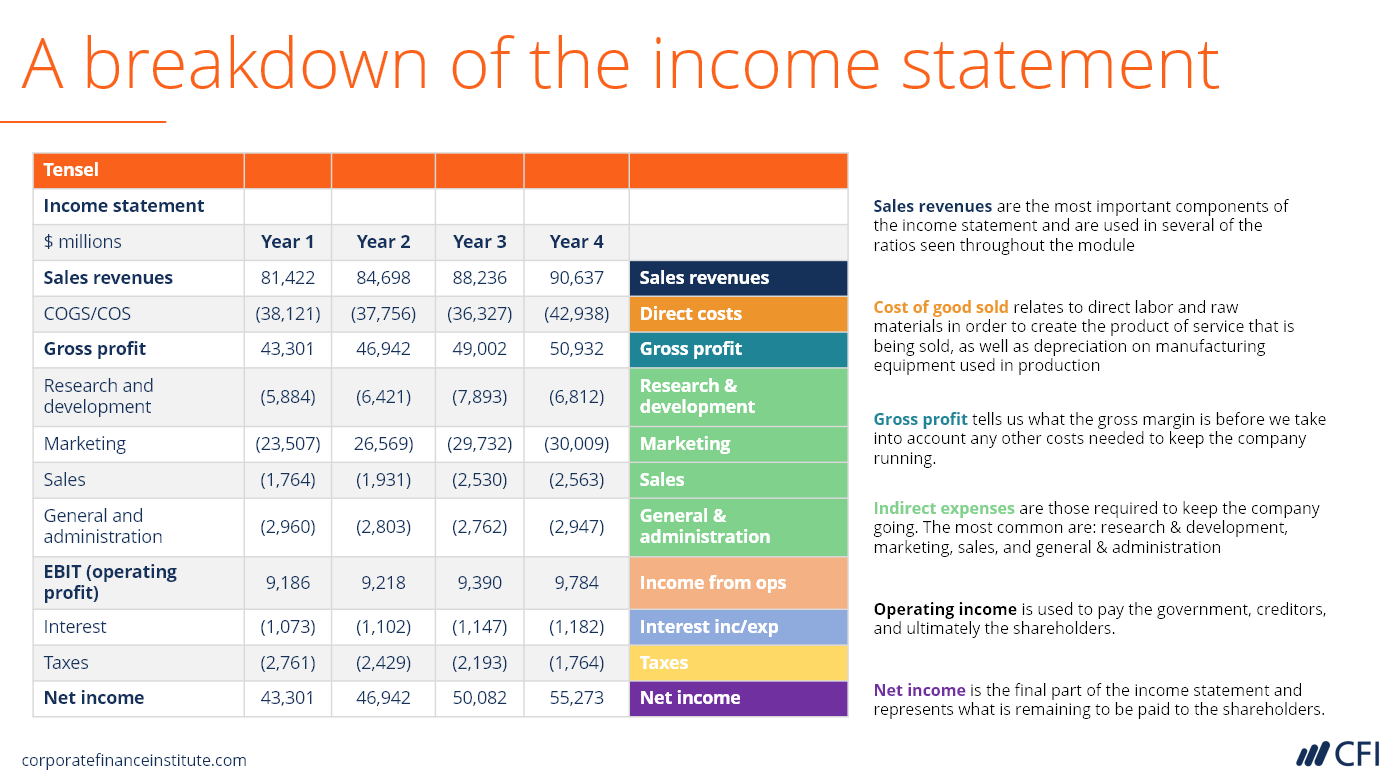

8️⃣ Accounting standards (US GAAP, IFRS, Canadian ASPE) for externally reported information require all product costs (direct labor, direct materials, variable and fixed overhead costs) to be included in the Cost of Goods Sold.

The difference between Revenue and Cost of Goods Sold is called Gross Margin.

9️⃣ Break Even analysis cannot be calculated using externally reported information.

It is an internal analysis performed by management accountants for internal management reporting purposes.

They ignore fixed costs in the calculation of profitability per product (Gross Margin), and instead use variable product costs only to calculate Contribution Margin.

Contribution Margin includes direct materials, direct labour, variable overhead, variable sales and marketing.

🔟 Your company calculates and uses the break-even point to make critical business decisions such as:

✅ setting product strategy (do we want to sell this product based on its profitability?)

✅ setting product pricing (what price should we sell this to cover costs and meet profit targets?)

✅ setting market strategy (can we operate profitably selling this product at this price level in this market?

Are Your Cash Flows Relevant?

Capital budgeting (CAPEX) projects will generate cash flows over several periods of time, but the trick is to only evaluate the relevant & incremental cash flows in your decision.

➡️ What cash flows are relevant?

Those cash flows that are unique for each separate capital budgeting decision and that will actually change in the future.

➡️ What cash flows are incremental?

Those changes in cash inflows and outflows which are directly attributable to investing in the project.

➡️ Here are the 4 types of cash flows you need to evaluate in any capital budgeting project:

1️⃣ Initial investment

✔️Capital expenditures - CAPEX

✔️Opportunity costs - benefits given up if an asset is used for one project instead of another

✔️Tax benefits from the acquisition of capital assets

2️⃣ After tax operating cash flows

✔️ Incremental revenues

✔️ Incremental costs

✔️ Tax effects

3️⃣ Working capital

✔️ Incremental working capital requirements during the project

✔️ Reduction of working capital requirements at the end of the project as receivables are collected, inventory is sold and suppliers are paid

4️⃣ Salvage values

✔️ Proceeds from sales or disposals of assets

✔️ Tax effects

🎯Remember a few important details:

✔️ use an after tax discount rate (WACC) for after tax cash flows

✔️ ignore sunk costs because they're not incremental to the project

✔️ financing costs are already part of the discount rate so don't double count

Is Your Cash Flow Statement Direct or Indirect?

Cash flow statements have 3 main sections:

➡️ Operating cash flows / Cash flow from operations

➡️ Investing cash flows / Cash flows from investing

➡️ Financing cash flows / Cash flows from financing

⚫ The only difference between the direct and indirect cash flow statements is how you calculate operating cash flows.

1️⃣ Calculating operating cash flows in the indirect method

✔️ start with net income from the Income Statement, which has been reported using accrual accounting

✔️ because the accrual income statement recognized revenues and expenses when they were incurred not when they were settled, it needs to be de-accrued to convert it into cash

✔️make adjustments for non-cash transactions such as depreciation and amortization, share based compensation, gains or losses from the sale of fixed assets or investments

✔️ make adjustments for non-operating items considered elsewhere in the cash flow statement (e.g. dividend payments received)

✔️ make adjustments for changes in current assets and current liabilities (receivables, payables, inventories, prepaids, accruals)

2️⃣ Calculating operating cash flows in the direct method

✔️ directly net cash collections and disbursements during the period

✔️ instead of reconciling the accrual income statement, directly consider cash based inflows and outflows from operations

✔️ add:

▪️net cash from customers

▪️cash paid to employees

▪️cash paid to suppliers

▪️cash paid for interest

▪️cash paid for taxes

⚫ Accounting frameworks offer a choice between the indirect and the direct method.

⚫ Most companies however choose the indirect method, because it’s faster, and thus cheaper.

Your Accounting Policies will drive your Income, your Cash Flow and your Valuation.

🎯 You have several areas where accounting frameworks allow you the flexibility to choose the accounting policy that best reflects your company’s circumstances.

🎯 Your accounting policy choices should also consider:

⚫ the risk management implications

⚫ the objectives of key stakeholders

⚫ the resulting impact on cash flow, earnings, financial ratios and covenants

🎯 You benefit from working with a professional accountant to ensure you’re making the right choices both from a technical as well as business standpoint.

⛔Here are 5 areas where the choice of accounting policy can have critical implications for a company’s Income, Cash Flow and financial ratios:

1️⃣ Revenue recognition:

The choice between the percentage of completion or completed contract method

2️⃣ Grant recognition:

The choice to reflect as other income, or net against relevant asset cost or expense amount

3️⃣ Inventory valuation:

The choice between average cost, FIFO, and LIFO (US GAAP only)

4️⃣ Taxation:

The choice between future/deferred income taxes and taxes payable (Canadian ASPE only)

5️⃣ Hedge accounting:

The choice of measurement method for determining the effectiveness of the hedge (probability of effectiveness, regression)

6️⃣ Provisions:

The choice of method for estimating the amount of the provision (expected value or likely outcome)

7️⃣ Depreciation:

The choice of method (straight line, units of production, declining/double declining balance). Further complicated by management estimates about useful life and salvage value.

10 Things you should know about Goodwill

What’s Goodwill anyway? And How does it work?

1. Goodwill is the residual value of an acquisition price after you accounted for the fair market values of your target’s tangible and intangible assets.

2. Goodwill is an intangible asset that represents the value of your company beyond its tangible assets and liabilities.

3. Goodwill is not something that you can separately buy or sell.

But you can built it over time, and sell it for $$$ in the future, alongside the business it helped you build.

4. Goodwill signals the presence of excess earnings.

That’s income above and beyond what you would required as a fair return on your business assets.

5. Goodwill is accounted for as a non-current intangible asset with an indefinite life.

You don’t depreciate it, but you do have to review it for signs of impairment annually or regularly, depending on accounting framework you follow.

6. Goodwill captures most of your business intangible value

The strength of your brand

The trust and loyalty of your customers

The reputation and image of your company

The executive capabilities of your management team

The competitive advantage offered by your patents, copyrights and industry expertise

7. Building goodwill typically requires a mix of business ethics, superior value and excellent customer service.

8. Destroying goodwill typically doesn’t take much.

The easiest way you can destroy goodwill is by prioritizing short-term gains over long-term reputation, and corporate profits over customer service and employee engagement.

9. Goodwill impairment charges will negatively impact your earnings, though they typically don’t also impact operating earnings.

As a non-recurring non-operating charge, they also typically won’t impact EBITDA or valuations.

To determine if the value of your goodwill is impaired, test if the acquired business is still projected to generate the incremental flows originally projected, or compare its market value with that of similar companies.

10. As long as it’s on your balance sheet, Goodwill will negatively impact your balance sheet leverage ratio, your returns on assets and equity, and your P/E ratio, to name a few.

That might complicate your ability to secure financing for your newly acquired subsidiary and may limit your growth potential, which in turn would reduce earnings and extend breakeven timeframes.

10 Things You Didn’t Know about Financial Analysis

1️⃣ There are 2 types of Financial Analysis:

🎯 Internal Financial Analysis uses internally available information and is geared towards planning and executing to achieve your company’s strategic objectives:

>> profitability, efficiency, liquidity

🎯External Financial Analysis uses externally available information and is geared towards evaluating the risk and return of investing or or lending to your company:

>> leverage, debt servicing, liquidity, solvency, returns

2️⃣ Different providers of capital have different metrics to assess and track the financial health of your business

Equity investors use earnings performance or market growth potential for stock and enterprise valuation.

In contrast, for a lender, income doesn't determine credit quality and market growth potential is not nearly as relevant as for an investor.

3️⃣ If your business cannot meet its debt obligations, your creditors will likely put the business out of business.

Financial obligations are repaid with cash, not with accounting-adjusted earnings metrics such as EBITDA.

4️⃣ External analysis will sensitize the internal analysis and overlay the impact of industry trends and economic conditions on top of your financial statements.

Your ratios need to align and track to how third parties calculate them.

5️⃣ Financial ratio benchmarks depend on numerous individual variables.

What might be considered a strong performance in one industry may be weak in another.

6️⃣ Accounting policy choices reflect the level of management aggressiveness.

How revenue, expenses, and debt obligations are recorded gives an indication of how aggressive management is, which will directly impact the perceived business risk, it’s ability to attract capital, and the cost and terms of capital attracted.

7️⃣ Not all leverage is created equal.

Assets deemed to be stable and with high cash generation potential can be leveraged more than assets of questionable value and cash flow.

8️⃣ Operating assets can be under or overvalued on the balance sheet.

For example, goodwill associated with a recent acquisition will inflate assets, while well-depreciated assets are often undervalued on the balance sheet.

9️⃣ An increase or decrease in profit margins may be indicating a fundamental shift in your business dynamics.

🔟 Previous performance may not be a good indicator of future performance.

To improve your financial analysis skills, check out the Corporate Finance Institute® (CFI)'s FA Fundamentals.

Do you know when to Capitalize and when to Expense?

Some next steps for you to consider:

Sponsor this newsletter, to promote your work and be of service to our highly engaged professional community made up of CFOs, CEOs, CPAs, MBAs, and other executive leaders.

Forward this newsletter, because if you enjoyed it, your network would probably enjoy it too. Send it to your friends and colleagues to share the knowledge. They'll appreciate you, and you will help inspire and support business professionals around the world to become strategic in their understanding and use of finance.

Subscribe to The Finance Gem 💎 to receive my newsletter in future, if this email was forwarded to you.

Thanks so much for reading. See you next week.